A huge amount of the discussion on recovery after COVID-19 is not truly global. It depends, as is so very often the case, upon views from the West about the West and on what might or might not emerge from the US economy. It seems that, after all, we have not learnt very much since 2008 and that financial recession. Thus, the focus remains on such elements as Western (read mostly USA, U.K, Germany and France) domestic economic policy surrounding unemployment and social welfare, productivity, rates of economic growth, and dimensions of national debt.

Most assumptions originate in the Atlantic rather than the Indian-Pacific oceans, and that is clearly misguided even in a narrow sense, as much of the US economy effectively lies in the sphere of the commercial interests of the Pacific, which conjoin Asia’s Far East and America’s Far West. Things change when we take a world view, which would emphasise the likelihood of fast East Asian growth and very troublesome American and European growth and probably stagflation, and the possibility of most of the rest of Asia following a path that does not depend upon the highways and slowdowns of the American economy.

This perspective does expose the myopia of the recent Biden Asian trip, and the attempt to get Japan on side against China, and India on side of US economic development, as possibly redundant or even mischievous from a global perspective. This is just the time to reduce the new expressions of east-west tension and to recognise the possibility of a New Cold War seriously upsetting all chances of both global recovery and improved incomes for poorer nations, especially in Asia.

The dampening potentials of the West

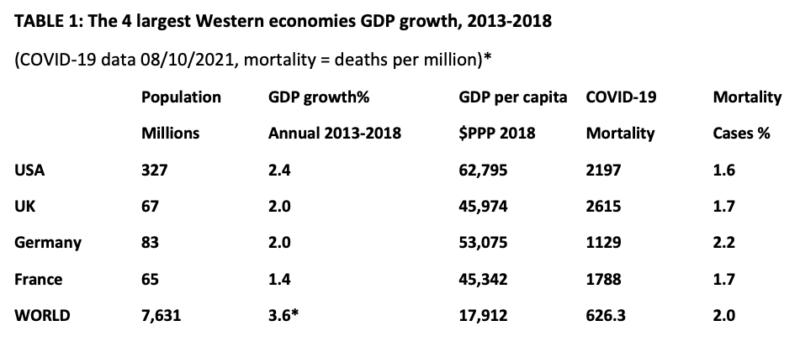

By mid-2021, it was abundantly clear that the largest of the Western nations, the ones that are pivotal to the future success of Atlantic-based recovery, had performed very badly in terms of both COVID-19 and overall economic growth.

Of the four major nations listed above and in Table 1 below, COVID mortality (deaths per million) ranged from 2,515 to 1129, against a background of very low GDP growth, an annual range for 2013-2018 of 1.4% to 2.4%.

*Sources: Pocket World in Figures 2022 Edition, The Economist, Profile Books; Worldometers

What seems very clear is that the most powerful of the Western economies are also those which before the pandemic had been growing at a rate well below the world average. The most powerful military and commercial systems of the US and UK were growing at barely half the rate of the world average since 2013. They were not a major source of world recovery after the crisis of 2008. Secondly, despite their enormous wealth as measured in USD, GDP per person adjusted for purchasing power parity (and so reflecting reasonably accurately comparative welfare between nations), they have all performed badly in terms of mortality from COVID-19 as measured in deaths from the inception of the pandemic in each country to the present time. Despite the enormous impact of vaccination in such rich nations, the overall mortality of these nations ranged from 1,129 deaths per million people in Germany to 2,615 in the UK by December 8, 2021.

From this, we may conclude that the richest Western nations may not be the focus of post-pandemic economic recovery. Most of their increased government expenditures and national debt during 2020 and 2021 have arisen from socio-economic rescue operations in the areas of health expenditure (well beyond that needed for COVID-19 directly as the latter had crowded out necessary medical treatment for all other diseases), food supplies to the poorer members of their societies, unemployment relief of a variety of kinds, policing of COVID regulations amongst individuals and the major institutions of health, education, and employment. Post pandemic policies in such nations will continue to focus on broadly short-term social welfare efforts, and control of expenditure in the public sectors as their governments strive to retain some degree of public trust and viability.

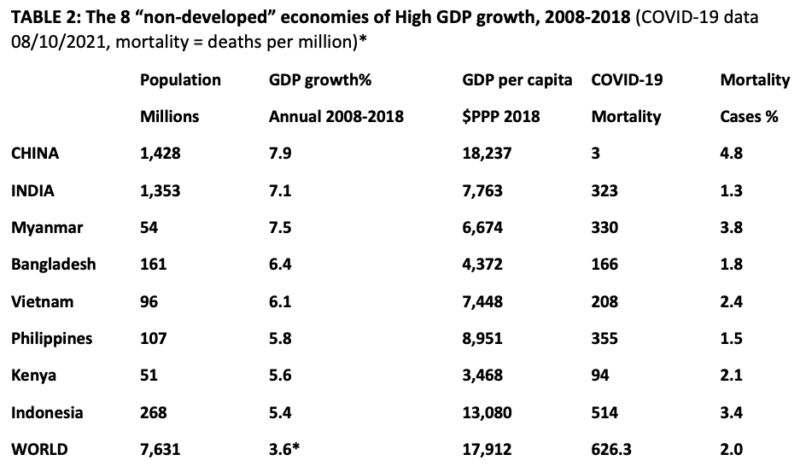

In contrast, the fast-developing nations of the Indian-Pacific Oceans region have all done much better in terms of COVID-19 mortality since the inception of the pandemic.

‘In China ‘s epidemic, there is a staff member on each street to check the temperature registration.’ Photo by cheng feng in Sichaun, used under Unsplash license.

If we consider as a comparable group the 7 “non-developed” Asian (plus Kenya as the nearest African comparator) economies of high GDP growth during 2008-2018 (China, India, Myanmar, Bangladesh, Philippines, Vietnam, Indonesia), then their range of GDP annual growth during 2008-18 was 7.9% (China) to 5.4% (Indonesia), and their range of COVID-19 mortality by October 2021 was 514 (Indonesia) to 3 (China) per million. They represent a huge demography of fast-growing, trading nations with relatively low levels of Covidity. It is a group that represents the sustained large-scale growth that has occurred since 2008 inside large, poorer nations but outside of the West and Japan. So, we have now devised a reasonable engine of global comparison.

Table 2 lists nations in order of magnitudes of Gross Domestic Product (GDP) growth, and only includes those with at least 5% annual rates of GDP growth since the financial crisis of 2007/8, each with over 50 million people at less than 20,000 USD per capita annual incomes. This basically covers the economies of fast growth but low income outside of Europe and the USA but excludes small systems of fast growth such as Qatar (2.8 million population) or systems whose growth was based on disastrously low levels of absolute income (e.g., Ethiopia with a 2018 purchasing power parity (PPP$) per capita income of only $2,022 USD). It, thus, represents the sustained large-scale growth that has occurred since 2008 in large, poorer nations outside of the West and Japan.

*Sources: Pocket World in Figures 2022 Edition, The Economist, Profile Books; Worldometers

An India-Pacific argument for our most probable post-pandemic economic scenario is made even stronger when we consider the potential role of East Asia, led by Japan and China. The differences exposed so easily within this group in the political arena (Taiwan viz China, Japan viz China, and so on), which employ a large fraction of the resources of our major news agencies and social media, are, in fact, less than the complementarities between themselves and the 7 nations isolated above. All have been growing fast over a significant period, all have been highly dependent on expanding trade and investments, all have benefitted from increased activity in their public sectors, and all have escaped the worst ravages of the pandemic. Whether this latter commonality itself derives from more efficient virus policy regimes in such nations when compared to our 4 Western leaders above is not our prime concern here. There is little doubt, however, that it must be a salient matter for future global policy analysis. It reflects a new version of the old (2004) Fukuyama thesis on “failed” or weak states.

This was untenable as any sort of equilibrium position long before COVID-19 struck the global system. As we shall recall again here, much growth after 2008 came from Asia and not from Europe or the US.

The prosperous East Asian nations (Japan, South Korea, Taiwan, Singapore and Hong Kong, as well as China at the lower income margins) have been the greatest assets for growth of the world system for some time now. This does not argue that they are perfect places, nor does it show that the growth disparities will remain long into the future. But the pandemic divergencies certainly suggest the existence of a virile Indian-Pacific Ocean Edge now at the centre of growth, composed primarily of the low-COVID nations of Table 2 above and the 5 additional East Asian economies. The trade complementarities between them, stability of governance, and general increases in economic/political freedom that embrace such different historical experiences as Kenya and China, although all debatable or problematic in their measurement, do not shape up badly when compared to slow-down, confusion and failure of COVID-19 policy regimes in the four major democracies.

The American dilemma: Aggressive foreign policy as a political distraction

This is the true — if somewhat complex — context of our argument for a new deal centred in the USA. In recent times much of US foreign policy has been a reaction to internal social and economic problems associated with low growth, failing productivity, and structural problems of foreign trade. This came to an obvious head with Donald Trump but can also be seen in the distraction and avoidance activities of all post-Clinton regimes. Presidents and their advisors may well know the underlying problems and the need for a more root-and-branch, more radical, domestic policy, but they have generally sought to avoid all moves towards a new deal through major distractions, the most effective of which tend to lie with changes or extensions of foreign policy. A cynic might suggest that the crisis centred in Ukraine is a godsend to the White House as long as it remains below the level of wholesale warfare involving US troops.

Of course, there is nothing new in some of this. In “Animal Farm” (1945), George Orwell posed the mythical destructive power of the excluded, erstwhile democratic leader pig, Snowball, as a foreign enemy, used by fascist pig Napoleon to distract from or justify his increasingly totalitarian grip on a failing farm economy. But generally, today’s foreign policy discourse assumes that it is some complex outcome of international games and strategies, perhaps especially so in democratic systems. As games and strategies are often open-ended, and as cheating is possible, this leads to a whole world of foreign policy expertise and pronouncement, much of which misses the real-world events as they happen — no one predicted the timing and character of the present Ukraine turmoil.

The major problem for the USA, of course, in managing real innovation from the White House is that the political weight of the Presidency is never in line with all of Congress, the Senate and the Supreme Court. No passage through of any important bill can ever be guaranteed, checks on anything “radical” are much bigger than balances. So foreign policy has become the easier rhetoric, if the most dangerous policy arena. High finance, powered by property investment and a mess of regulation combines reasonably well with militarism, tending to floor serious discussions of the flaws in the underlying political economy.

Thus, the impossibility of removing by presidential legislation such obvious negative elements in the USA as the gun lobbyists, the agricultural interests, and the oil giants, these alone ensuring that American democracy is seriously flawed, both in itself and as the political vehicle for economic equity and increased social welfare. Whatever his liberal agenda, Obama was felled in his tentative moves to address the “Minsky moment” — where careless and hitherto cushioned indebted investors offload stocks quickly in order to meet loans, forcing markets down — a commanding feature of present financialisation.

US politics as a limiting factor in global dynamics

But the global need for an American-centred new deal is obvious at this juncture. The above interpretation of the patterns of likely global recovery requires the development of trade and investment patterns that are secure. The basically false character of the media-centred dualism of East versus West is clear (viz the realities of global trade and investment) and incompatible with long-term global health. An American regime that turns away from aggressive and chauvinistic foreign interventions or provocations in favour of a radical socio-economic reform agenda will at once be acting for the betterment of its own civil society and to much more stable global economic growth. However, the incorporation of such a refreshing perspective into policy and new legislation is a matter more purely political. If students of economics ever needed evidence of the complexity of a true political economy, then they have it now, smack bang in the middle of all the problems of global civil society.